Retirement Planning – SOLO 401K

In our wealth management practice, we emphasize using your “now” money to make smart financial decisions for today and for well into the future. We have even been known to make negative comments about financial instruments that make it hard to access your money before, say, age 59.5. It’s not that these instruments are bad in themselves, we just don’t want them to be your default retirement strategy without some thought put into them.

In our wealth management practice, we emphasize using your “now” money to make smart financial decisions for today and for well into the future. We have even been known to make negative comments about financial instruments that make it hard to access your money before, say, age 59.5. It’s not that these instruments are bad in themselves, we just don’t want them to be your default retirement strategy without some thought put into them.

So, yes, there is absolutely a place for retirement instruments like IRAs and 401(k)s in a well-rounded retirement (or time freedom) plan. Which brings me to the Solo 401(k.) It is unique and checks a lot of boxes for us in terms of tax advantage AND access to your money when it makes sense.

The Solo 401(k) if for the true solopreneur. If you are considering or likely to hire even one employee beyond your spouse in the future, the SEP-IRA is the better choice. But if not, a Solo 401(k) has a lot of advantages.

If you are in a situation where you own a business and have a few employees, or are likely to in the future, you might want to know more about the SEP. I outlined the details about the SEP-IRA in this previous article, which is worth checking out <link>.

Beyond the employee factor, there are other reasons a Solo 401(k) might be attractive as a retirement savings vehicle. Like an employer-sponsored 401(k), a Solo offers some of the same features. Unlike the SEP, catch-up contributions are allowed for those age 50 and older. You can also take out a loan on your Solo 401(k) of amounts under $50,000 or 50% of your account balance, whichever is the lower dollar amount. If you have followed our work, you have heard about our Uncommon Banking approach to using the cash value of a whole life insurance policy to take out a loan. While the Solo 401(k) is a similar approach, there are fewer hoops to jump through in giving yourself a loan through a whole life policy. All that being said, this loan potential is a solid benefit of having the Solo 401(k) as opposed to an IRA.

Also, unlike a SEP-IRA, there are Roth options for a Solo 401(k) as well, so you can choose to pay income tax now, and then take tax-free withdrawals when you are in retirement.

Opening a Solo 401(k)

Starting a Solo 401(k) is a little more complex than a SEP-IRA, but still a manageable process. If you have an EIN (employer identification number) you can open an account at most any online brokerage. We help walk people through the process all the time.

Eligibility and Limits

Anyone who generates net profits from a sole proprietorship, LLC or other business organization can open a Solo 401(k) as long as they have no employees aside from their spouse.

Here are the limits as detailed by the IRS:

Contribution limits for self-employed individuals

You must make a special computation to figure the maximum amount of elective deferrals and non elective contributions you can make for yourself. When figuring the contribution, compensation is your “earned income,” which is defined as net earnings from self-employment after deducting both:

- one-half of your self-employment tax, and

- contributions for yourself.

Contribution limits are similar to the SEP IRA. Individual limits are set at $57,000 for 2020 and $58,000 for 2021. You can then contribute as both an employee and employer. As an employee, you can put up to $19,500 away, or 100% of your income, whichever is lower. If you are over 50, you can contribute an additional $6,000 catch-up amount.

As an employer, you can put away an additional 25% of your compensation or net self-employment income, which is your net profit less half your self-employment tax and the plan contributions you made for yourself, up to that total of $57,000 or $58,000.

Choose Your Tax Advantage

You can choose a traditional 401(k) in which contributions reduce your taxable income in the year contributions are made, or the Roth option where you will pay taxes on contributions as regular income, but will be able to take disbursements tax-free in retirement.

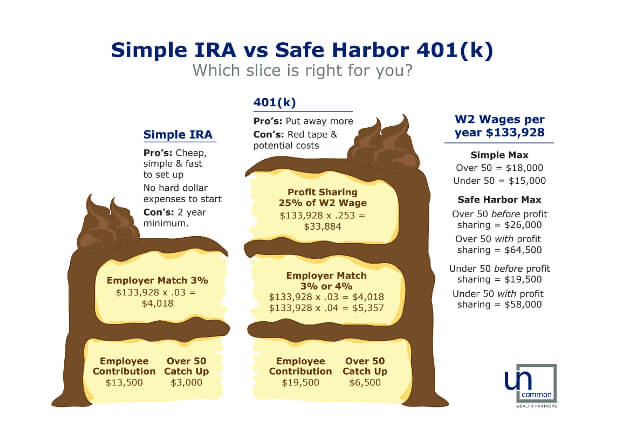

Here is a comparison of a 401(k) plan with a SIMPLE IRA

If you are self-employed, the Solo 401(k) has a lot going for it. It is flexible, the limits on contributions are high, you can loan yourself money from it, and choose your tax advantage.

Let us know if we can answer any questions you have or help you get a Solo 401K set up.