Retirement Planning – Safe Harbor 401K

Among the many plans, we help clients with, the safe harbor 401(k) is the most popular plan for small businesses. There are several reasons for this, including generous contribution limits and profit-sharing options. Let’s take a closer look at how the safe harbor 401(k) works.

Among the many plans, we help clients with, the safe harbor 401(k) is the most popular plan for small businesses. There are several reasons for this, including generous contribution limits and profit-sharing options. Let’s take a closer look at how the safe harbor 401(k) works.

To achieve safe harbor status, a 401(k) plan needs to meet certain contribution and participant disclosure requirements.

According to the IRS:

“Employers sponsoring safe harbor 401(k) plans must satisfy certain notice requirements. The notice requirements are satisfied if each eligible employee for the plan year is given written notice of the employee’s rights and obligations under the plan and the notice satisfies the content and timing requirements.”

“In order to satisfy the content requirement, the notice must describe the safe harbor method in use, how eligible employees make elections, any other plans involved, etc.”

ERISA laws require that safe harbor 401(k)s complete tests to confirm they do not discriminate in favor of Highly Compensated Employees (HCEs) or exceed IRS contribution limits.

Understanding Employer Contribution Requirements

Employers have two options, match based or non-elective based plans. A basic match is a 100% match on the first 3% of deferred compensation plus 50% on deferred compensation between 3% and 5%. You could opt for an enhanced match, which is often a 100% match on the first 4% of deferred compensation.

For non-elective based plans, eligible employees receive an annual employer contribution of 3% of their salary. This amount is immediately fully vested and the employee gets it whether or not they contribute to the plan.

For plan years beginning after December 31, 2019, only match-based safe harbor 401(k) plans are subject to a participant disclosure requirement. As of this writing, non-elective based safe harbor plans are exempt.

As long as you as an employer follow the rules, and if, as an employee, you don’t mind that your money will be untouchable before you turn age 59.5 without penalty, the safe harbor 401(k) is a strong choice for both business owner and employee.

Comparing the Match

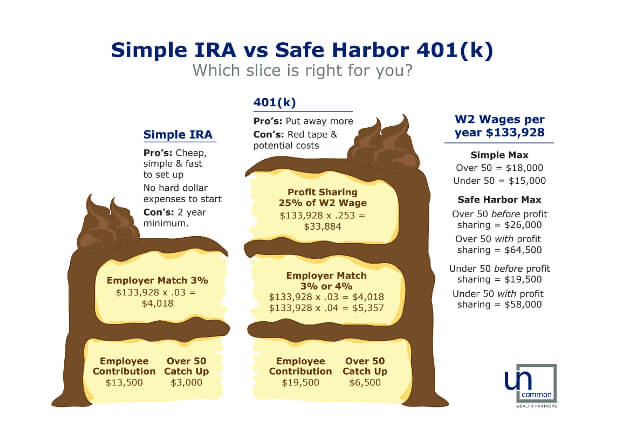

The chart below shows the differences between contributions to an IRA and a safe harbor 401(k). So for a person earning the dollar amount in the example of $133,000 per year can put away much more in the 401(k). Especially if a company takes advantage of the profit-sharing option and employer match, an employee under age 50 can put up to $58,000 into the retirement plan. For employees over age 50 and including the catch-up amount, you could squirrel away up to $64,000. That’s a significant advantage over the IRA max of $15,000 to $18,000.

We have some excellent ways to help clients with a safe harbor 401(k). They are great if you have an existing plan. We can review the plan design, look at how you are managing limits, and we can reduce the fees you are paying if you have over $500,000 in assets. The safe harbor 401(k) is designed to maximize owner directed profit sharing.

If you would like a quote or proposal, we would love to schedule a conversation with you.